Your house is worth $487,000.

Your bank

still says no.

Sell it. Stay in it. Walk out with the equity. We review every company that promises this — and we name the ones that got sued.

You're not the only one.

Every week, 20,000 American homeowners fall behind on a mortgage payment. Four kitchen tables. Same conversation.

APRs hit 24% and your bank called it a "product."

Credit card rates cracked 24% in 2025. A HELOC at 9.5% is just the same trap with a longer rope. There's a third option your bank won't mention.

Show me the third option

The clock started the day you opened it.

A sale-leaseback can close in 30 days. Here's the Monday-morning checklist every foreclosure attorney wishes their clients had seen a week earlier.

Read the 30-day playbook

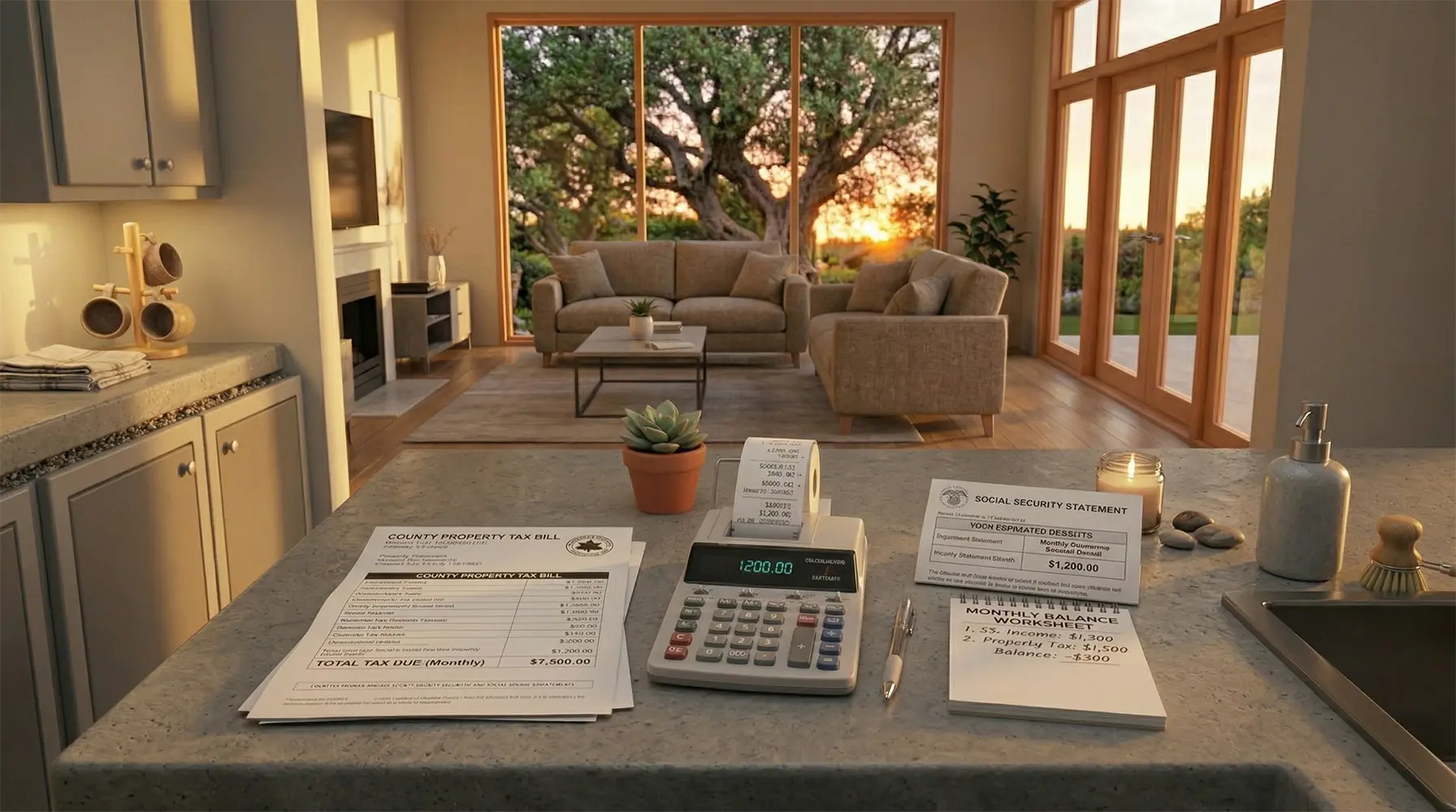

You own a $600,000 home. You can't cover property tax.

Moving out isn't the only move — and "reverse mortgage" isn't the only answer. Here's what retirees who stayed in their homes did instead.

Show me what retirees actually did

Neither of you wants to leave the school district.

Splitting the house doesn't have to mean handing it to a stranger on Zillow. There's a way to cash out and keep the keys in the same mailbox.

Read the divorce playbookTwenty years ago, nobody told you this option existed. We will.

— The Leaseback.com editorial team

A sale-leaseback in three steps.

Fortune 500 companies do it with office towers. Walgreens did one for $5 billion. Homeowners just weren't invited — until now.

01

01

To an investor. No bank. No loan. No interest. No credit check required. Cash offer in days.

02

02

Keep living in it. Same address. Same keys. Same mailbox. Fixed rent — no surprises.

03

03

As cash. Not a line of credit. Not a HELOC. Real money in your bank account.

Three enemies. Name them before you fight them.

Average HELOC APR in 2026: 9.5%. Average 30-year mortgage: 7.2%. The math on "just borrow more" stopped working in 2022, and your loan officer knows it.

Source: Federal Reserve H.15 →A second mortgage with a variable rate and a marketing budget. If rates rise, your payment rises with them. If you miss a payment, the house is still on the table.

Source: CFPB HELOC guide →Trade your 3% pandemic-era mortgage for 7.2% today — just to touch the same equity. Your payment balloons for 30 years. Miss it and they foreclose faster than any HELOC.

Source: CFPB Cash-out ReFi Guide →Four doors. One of them actually leads out.

| Your bank | HELOC | EasyKnock-style | Sale-leaseback done right | |

|---|---|---|---|---|

| Adds more debt | YES | YES | NO | NO |

| Needs a credit score | YES | YES | NO | NO |

| Monthly payment to a lender | YES | YES | Rent, variable | Rent, fixed |

| You keep the house | Until you miss a payment | Until you miss a payment | Until they said so | On a real lease |

The column where the duck says what the lawyers won't.

Send this page to someone who needs it. They'll owe you a coffee.